Applying for retirement involves submitting an application to your pension administrator, employer, or government agency—whichever manages your retirement benefits. The process typically requires filling out formal paperwork, providing proof of age and service, and waiting for approval before your benefits begin. For example, someone retiring from a 30-year career at a manufacturing company would contact their pension department, complete the retirement application form, submit documentation like a birth certificate and employment records, and then wait 2-4 weeks for the pension office to process the claim and determine their monthly benefit amount. The exact process varies significantly depending on where your retirement income comes from. If you’re drawing from a traditional pension plan, the process is managed by your former employer or a pension board.

If you’re relying on a 401(k) or IRA, you’ll work with the financial institution holding those accounts. Social Security retirement benefits require a separate application through the government. Most people need to coordinate multiple applications simultaneously—Social Security, any employer pensions, and personal retirement accounts—each with different timelines and requirements. Starting the application process too late can cost you money in missed benefits. Most plans allow you to apply up to four months before your intended retirement date, but some have earlier deadlines. Waiting until after you’ve already stopped working can delay your first payment by several months, leaving you without income while your application processes.

Table of Contents

- When Should You Apply for Retirement and What Makes You Eligible?

- Gathering Documentation and Meeting Application Requirements

- Understanding Your Benefit Options and Elections

- The Step-by-Step Application Process and Timeline

- Common Problems and Issues That Delay Approval

- Optimizing Your Application and Maximizing Benefits

- Post-Application and Moving Forward Into Retirement

- Conclusion

- Frequently Asked Questions

When Should You Apply for Retirement and What Makes You Eligible?

You can typically apply for retirement any time after reaching your plan’s minimum retirement age, which varies by program. Most employer pension plans allow retirement at age 55 to 62, though some require you to have worked a certain number of years. Social Security retirement benefits can begin as early as age 62, but you’ll receive a permanently reduced amount if you claim before your full retirement age (which ranges from 66 to 67 depending on your birth year). The trade-off is significant: claiming at 62 instead of waiting until 70 can reduce your lifetime Social Security income by 25 to 35 percent.

Eligibility requirements differ dramatically between programs. For a traditional employer pension, you typically need to have worked there for a minimum period—often 5 to 10 years—though some government and union pensions require 20 years or more. Social Security requires you to have earned at least 40 credits over your work history (roughly 10 years of covered employment). IRAs and 401(k)s have different rules: you can generally access 401(k) funds penalty-free at age 59½, but withdrawing earlier means paying a 10 percent penalty plus income tax on most distributions. Some plans offer early retirement options with actuarial reductions, meaning you’ll receive a smaller monthly payment if you retire before your full retirement age.

Gathering Documentation and Meeting Application Requirements

Before you submit any retirement application, you’ll need to collect specific documents. Standard requirements include a government-issued photo ID (like a passport or driver’s license), proof of your birth date (birth certificate), Social Security number, and documentation of your work history. If you’re applying for a pension, your employer should provide a statement showing your years of service and the vesting schedule that determines whether you’ve earned the full pension benefit. Many employers now provide this online through their benefits portal.

A significant limitation is that some documents take weeks to obtain. If you’ve lost your birth certificate, getting a replacement from your state can take 4 to 6 weeks, especially if you order by mail. Social Security applications require original or certified copies of documents, not photocopies, so you can’t simply scan and email things. This is why retirement planning experts recommend gathering these documents 6 to 12 months before your intended retirement date. One common mistake happens when people update their name (through marriage or legal change) but don’t update their Social Security account to match; this mismatch can block or delay benefit approvals, and correcting it requires submitting additional documentation to SSA.

Understanding Your Benefit Options and Elections

When you apply, you’ll need to make critical choices about how to receive your benefits. For employer pensions, you typically choose between a single-life annuity (you receive the full monthly amount but benefits stop when you die) or a joint-and-survivor annuity (you receive slightly less monthly, but your spouse continues receiving a percentage after your death). This decision is permanent—you can’t change your mind after payments begin. A 65-year-old worker with a $2,000 monthly pension might receive $2,000 as a single-life option but only $1,750 as a joint-and-survivor option, yet that $250 difference over 20 years represents $60,000 in lost survivor protection.

Social Security offers similar trade-offs. If you’re married, you need to decide whether you’ll claim on your own work history or, if you’re over full retirement age, claim a spousal benefit. A lower-earning spouse might receive more money by claiming a spousal benefit (up to 50 percent of the higher-earning spouse’s full retirement age benefit) than by claiming on their own record. Divorced individuals who were married for at least 10 years can claim on an ex-spouse’s record, even if the ex hasn’t applied yet—but only after age 62, and only if the divorce was finalized at least two years earlier. Many divorced people don’t realize this option exists, costing themselves thousands in foregone benefits.

The Step-by-Step Application Process and Timeline

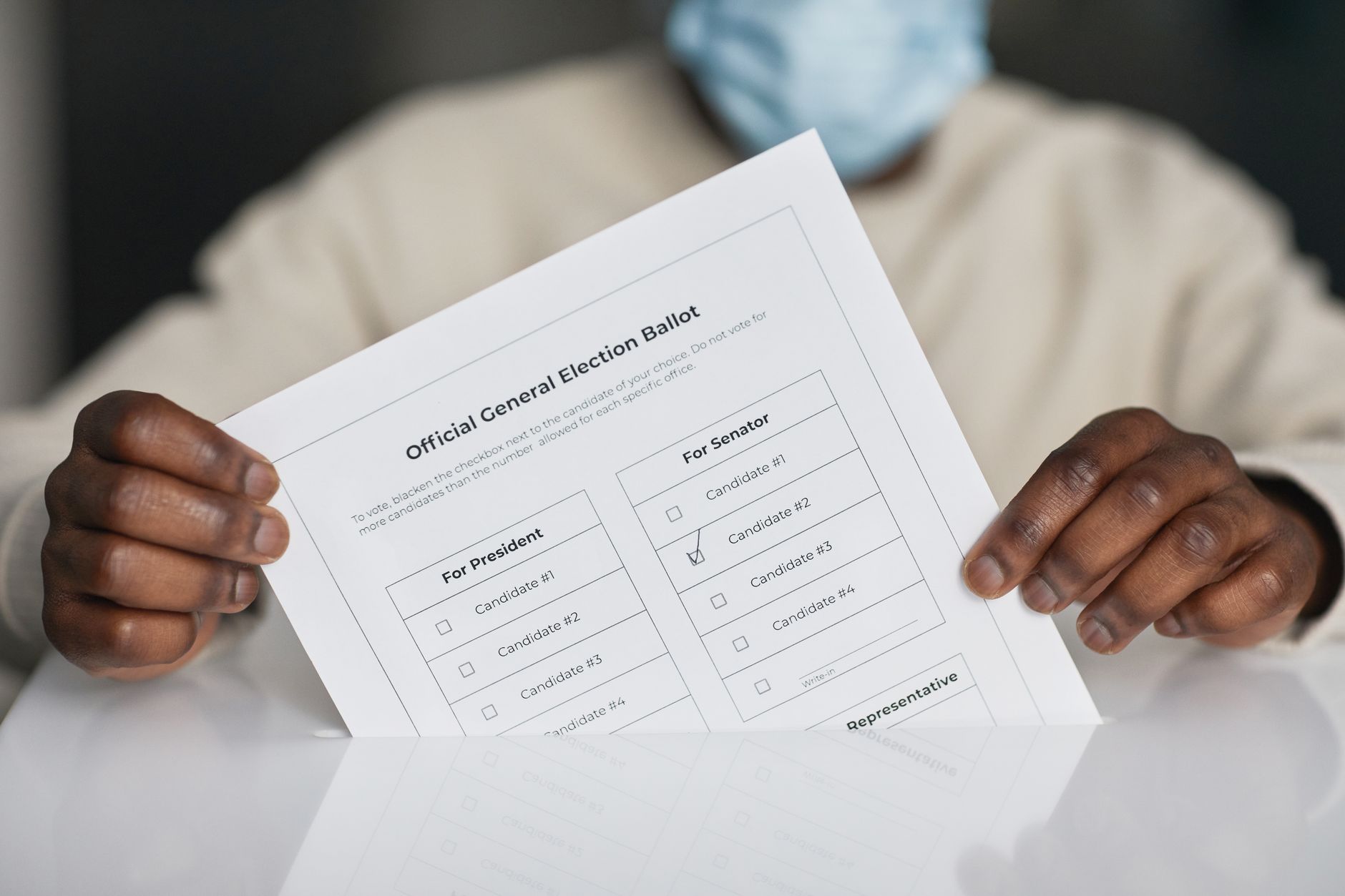

Start by contacting your pension administrator, employer, or the Social Security Administration to request your application materials. You can apply for Social Security online at ssa.gov, by phone at 1-800-772-1213, or in person at your local Social Security office. For employer pensions, contact your company’s HR department or benefits office. Most employers now have online portals where you can submit applications directly; if not, they’ll mail you paper forms. Fill out all required fields completely—incomplete applications are returned for correction, adding another week or two to the timeline. Submit your completed application along with all required documentation.

Keep copies of everything you send. If submitting by mail, use certified mail with return receipt so you have proof of delivery. Once received, the processing time typically ranges from 2 to 4 weeks for employer pensions, though government pensions can take 6 to 8 weeks. Social Security typically processes applications within 3 to 5 business days if you apply online, but paper applications can take significantly longer. Plan to apply at least 4 months before your intended retirement date to avoid gaps in income. If you’re retiring at the end of a month, submit your application in the previous month or earlier to ensure approval before your last paycheck arrives.

Common Problems and Issues That Delay Approval

The most frequent cause of delays is incomplete documentation. Missing a birth certificate or Social Security card copy sends applications back to the applicant, resetting the processing clock. Name mismatches between your documents and your employer’s records are surprisingly common—if your birth certificate shows your name as “Mary Elizabeth Jones” but your employer’s system has you listed as “Mary E. Jones,” this discrepancy can trigger manual review and delays. The solution is ensuring all your official documents are consistent months before applying.

A more serious issue arises with pension records disputes. Occasionally, an employer’s records of your employment dates or years of service don’t match what the employee remembers. Resolving these requires providing documentation like old paystubs, employment letters, or tax records—the search itself can take months if records were destroyed. Limited benefit vesting is another trap: an employee who worked somewhere for 4 years and 11 months might not be vested and therefore receives no pension at all, despite nearly meeting the 5-year requirement. Understanding your vesting schedule before applying prevents this painful surprise. Additionally, if you’ve worked for multiple employers, each pension or 401(k) requires a separate application and has its own processing timeline; coordinating these can extend your overall timeline by several weeks.

Optimizing Your Application and Maximizing Benefits

Before submitting, request a benefit estimate from each program to understand your payment amounts under different claiming scenarios. For Social Security, create a “my Social Security” account and review your earnings record—errors here directly reduce your benefits. If you spot missing years or incorrect amounts, request a correction immediately; fixing errors after you’ve already claimed benefits is extremely difficult. For employer pensions, request a detailed benefit calculation showing what you’ll receive at your chosen retirement date; verify the math independently using your plan’s published formulas.

Consider coordinating your Social Security claim with your pension timeline. If your pension plan allows you to retire at 62 but Social Security gives you a much larger benefit at 70, you might retire from work at 62 while delaying your Social Security claim, using pension income to bridge the gap. This strategy only works if you understand the penalties and delayed retirement credits—the math is complex enough that consulting a financial advisor often pays for itself. Some employers offer “window” early retirement programs with enhanced benefits during specific periods. If you qualify, calculate whether accepting the enhanced early retirement benefit beats working longer to increase your standard pension.

Post-Application and Moving Forward Into Retirement

Once approved, your first benefit payment typically arrives either in the same month you apply or the following month, depending on the program and payment method. Social Security deposits benefits on specific dates based on your birth date; employer pensions usually align with your company’s payroll schedule. Set up direct deposit to avoid delays from mailed checks. Your first payment will likely be smaller than subsequent ones because it’s prorated for the partial month.

After retirement approval, stay vigilant about maintaining your benefits. Social Security requires you to report significant life changes like remarriage, working after claiming, or relocating internationally. Pension administrators need to know if your contact information changes or if you’ve elected a survivor benefit and your spouse passes away. Many retirees ignore these notification requirements, creating complications years later when discrepancies are discovered during routine audits. Understanding that retirement approval is the beginning, not the end, of your relationship with these agencies helps you protect the income you’ve worked decades to secure.

Conclusion

Applying for retirement is a multi-step process that demands attention to detail and forward planning. Whether you’re tapping a pension, Social Security, 401(k), or some combination, each program has distinct eligibility rules, documentation requirements, and benefit options that dramatically affect your lifetime income. Starting your application process 4 to 6 months before your intended retirement date allows time for document gathering, corrections, and processing delays without leaving you stranded without income.

The decisions you make during the application process—particularly whether to claim benefits early, which payout option to select, and how to coordinate multiple programs—will shape your retirement finances for the next 20 to 30 years. Take time to understand your options, verify all information for accuracy, and consider consulting a financial advisor if your situation involves complex choices like spousal benefits or multiple pensions. Your application marks the moment when decades of work begin to pay off; making sure it’s done correctly ensures that payout is uninterrupted.

Frequently Asked Questions

How far in advance should I apply for retirement?

Apply at least 4 months before your intended retirement date. This timeline allows for document gathering (which can take weeks), mail delivery, processing time (2 to 4 weeks for most plans), and corrections if anything is incomplete or incorrect. Applying this far ahead prevents gaps in income between your last paycheck and your first retirement benefit.

Can I apply for Social Security and a pension at the same time?

Yes, but they’re separate applications. Social Security is a federal program processed by the SSA, while pensions are managed by your employer or pension board. Coordinate the timing so both applications align with your retirement date, but understand each has its own processing timeline and requirements.

What happens if my application is denied?

The denial notice explains why. Common reasons include incomplete documentation, unmet vesting requirements, or eligibility issues. You have the right to appeal most denials; the appeal process involves submitting additional documentation or evidence and typically takes 2 to 4 months. For Social Security denials, request a reconsideration within 60 days of the denial notice.

Can I work while applying for retirement benefits?

This depends on your age and the program. Before your full retirement age, earning above a certain limit (about $22,000 annually for 2024) reduces your Social Security benefits by $1 for every $2 earned over the limit. Pensions typically allow continued work without penalty. Carefully check your plan’s rules before planning to work part-time in early retirement.

What documents do I absolutely need?

At minimum, have a certified birth certificate, government-issued photo ID, and Social Security card or number. For pensions, add proof of employment (recent paystub, employee ID, or employment letter). Original or certified documents are required; photocopies are rejected. Start gathering these at least 6 months before applying.

If I miss the application deadline, can I apply late?

Most programs allow late applications, but your benefits don’t start retroactively from your original eligibility date. Generally, Social Security allows retroactive payment for up to 12 months before your application date, but you lose all earlier benefits. Pension plans typically don’t offer retroactive payments, so a late application means a permanent loss of months of benefits. Never delay applying once you’re eligible.